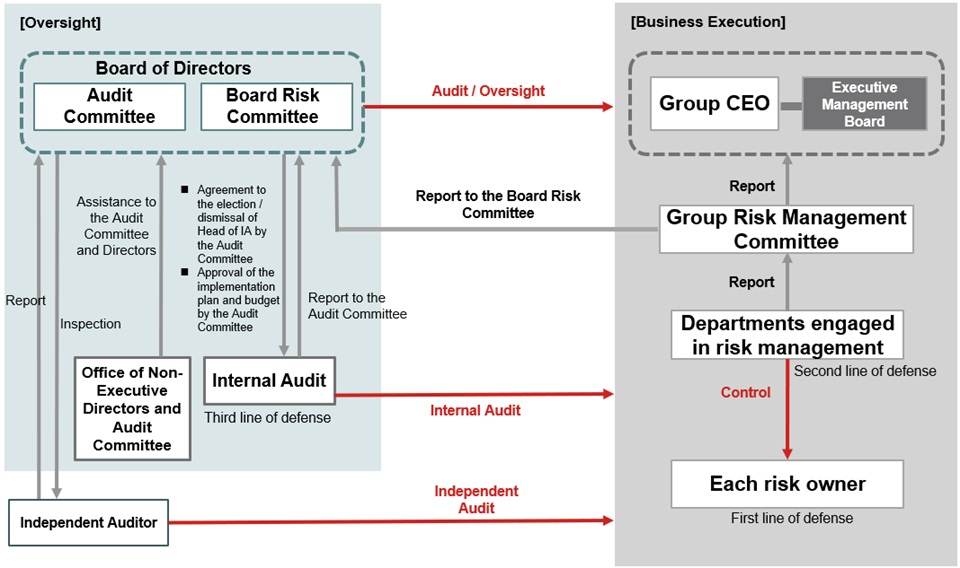

Nomura Holdings is committed to strengthening and improving our internal controls system to promote proper corporate behavior throughout the Nomura Group, from the viewpoints of ensuring management transparency and efficiency, complying with laws and regulations, controlling risks, ensuring the reliability of business and financial reports and fostering the timely and appropriate disclosure of information. In addition to risk management conducted by first line of defense (business divisions) and second line of defense (Risk Management and Compliance etc), the third line of defense (Internal Audit) conducts internal audits independently from business execution to ensure the effectiveness and appropriateness of internal controls across the Group’s operations. ("Three Lines of Defense" approach).

As a company with a nominating committee system, etc., the core role of management oversight is carried out by the Board of Directors and the Audit Committee, both of which have a majority of outside directors. To ensure the appropriateness of the Group’s operations, the Board of Directors monitors the development and operation of the internal control system by Executive Officers and requests improvements when necessary. The Chair of the Board of Directors is held by a Director who is not concurrently serving as an Executive Officer, allowing the Board of Directors to monitor the development and operation of the internal control system by Executive Officers and request improvements as necessary. In addition, the Audit Committee audits the legality, appropriateness, and efficiency of the execution of duties by Directors and Executive Officers to ensure the appropriateness of the Group’s operations, and by appointing an outside director as chairperson, the independence from business execution is further clarified.

The Audit Committee receives direct reports from the Executive Officer in charge of internal audit (Group Internal Audit Head) regarding the development and operation of the internal audit system, the status of internal audits, and important matters and trends related to overall internal controls identified through internal audit activities. Any matters worthy of special attention are included in the regular reporting provided by the Audit Committee to the Board of Directors.

In addition, to strengthen the independence of the internal audit sections from the business execution functions, the annual internal audit plan, budget formulation and changes, and the setting of performance objectives for internal audit require the approval of the Audit Committee. When formulating the annual internal audit plan, the Audit Committee requests the Group Internal Audit Head to prepare the plan based on key audit focus areas identified as priorities going forward. The appointment and dismissal of the Group Internal Audit Head also requires the consent of the Audit Committee.